Ridesharing services have transformed how Californians navigate their cities, from Los Angeles to San Francisco. With Uber holding 76% of the U.S. rideshare market, its presence is undeniable. However, this convenience introduces a layer of complexity when an accident occurs. An Uber accident isn't just another car crash; it involves a tangled web of personal auto insurance, corporate commercial policies, and specific state regulations. For Uber drivers, passengers, and other motorists, understanding who pays for bodily injury, property damage, and medical expenses is critical but often confusing.

Why Uber Accidents Are Different: Navigating Complex Insurance Policies

Unlike a typical two-car collision where drivers exchange their personal insurance information, an Uber accident involves multiple potential layers of coverage. The applicable insurance policy hinges almost entirely on the Uber driver's status within the Uber app at the exact moment of the crash. Was the driver offline, waiting for a ride request, en route to a pickup, or actively transporting a passenger? Each phase triggers a different level of liability coverage, creating a complex claims environment that can be difficult to navigate without clear guidance.

What This Guide Will Cover: Your Essential Road Map

This guide serves as a comprehensive roadmap for anyone involved in an Uber accident in California. We will break down Uber's intricate insurance system, clarify who is liable in various scenarios, and provide a step-by-step plan for what to do immediately after a crash. From filing an Uber accident claim to understanding your legal rights under California law, this article will equip you with the knowledge needed to protect your interests and pursue fair compensation.

Understanding Uber's Insurance Coverage in California

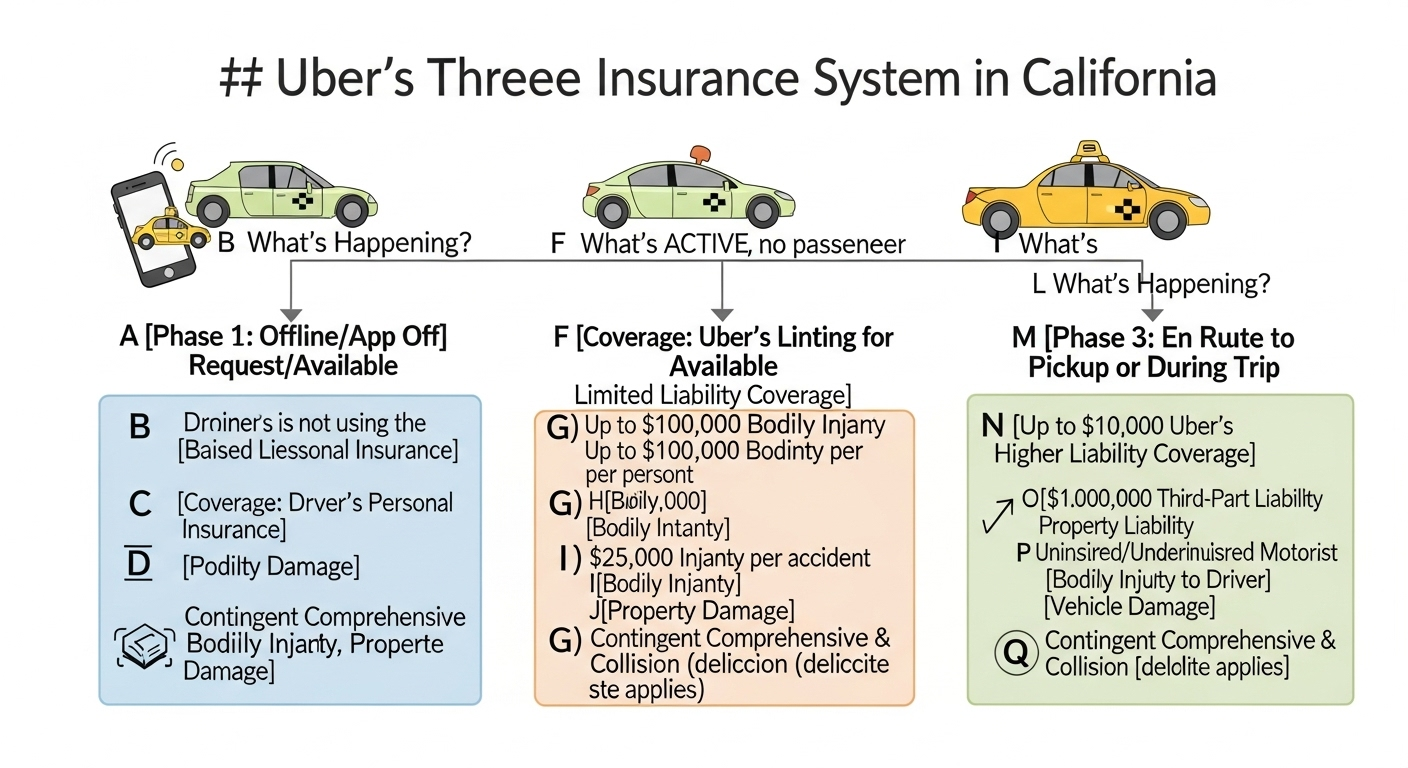

Uber's insurance coverage varies depending on the driver's status within the app.

At the heart of any Uber accident claim is the company's insurance program. It's designed to work in conjunction with, and often supersede, a driver's personal policy, but only when the driver is working.

The Crucial Difference: Uber's Commercial Coverage vs. Personal Auto Insurance

A standard personal auto insurance policy is designed for non-commercial use. In fact, most personal policies contain a "business-use exclusion," meaning they will deny claims if an accident happens while the driver is engaged in commercial activity, such as driving for ridesharing services. To fill this gap, Uber provides a commercial auto insurance policy for its drivers. This policy provides third-party liability coverage, but its activation and coverage limits depend entirely on the driver's activity in the app.

Uber's Three-Phase Insurance System for Drivers and Passengers

California law and Uber's policies create a three-phase system that dictates which insurance coverage applies during an Uber driver's shift. Understanding these phases is crucial for both Uber drivers and anyone else involved in a collision.

- Phase 0: App is Off. When the Uber app is off, the driver is considered off-duty. In this situation, only the driver's personal auto insurance policy provides coverage. Uber's insurance offers no protection.

- Phase 1: App is On, Driver is Awaiting a Request. The moment a driver logs into the app and is available to accept rides, a limited level of Uber's third-party liability coverage kicks in. This includes $50,000 for bodily injury per person, $100,000 for bodily injury per accident, and $30,000 for property damage per accident, as mandated by California law. This coverage applies if the driver's personal insurance doesn't.

- Phases 2 & 3: Driver Accepts a Ride and During the Trip. Once a driver accepts a ride request and is en route to pick up the passenger (Phase 2) or has the passenger in the vehicle (Phase 3), Uber's full insurance coverage is active. This includes $1 million in third-party liability coverage. This substantial policy also provides uninsured/underinsured motorist (UM/UIM) bodily injury coverage and contingent collision coverage for the Uber driver's vehicle (subject to a deductible).

Who is Liable? Determining Fault and Coverage in a California Uber Accident

California operates under an "at-fault" insurance system, meaning the person or party responsible for causing the accident is also responsible for the damages. In an Uber accident, determining liability dictates which insurance policy will respond to the claim.

When the Uber Driver is At Fault (During an Active Trip)

If an Uber driver causes an accident during Phase 2 or 3 (en route to a passenger or during a trip), Uber's $1 million third-party liability insurance policy is the primary source of compensation for injured parties. This includes covering medical bills, property damage, and pain and suffering for Uber passengers, pedestrians, cyclists, or occupants of other vehicles.

When Another Driver is At Fault for the Uber Accident

If another driver crashes into the Uber vehicle and is found to be at fault, the at-fault driver's auto insurance is the primary source for damages. However, if that driver is uninsured or has insufficient coverage to pay for the injuries to the Uber driver and passengers, Uber's Uninsured/Underinsured Motorist (UM/UIM) coverage can be triggered to cover the shortfall.

When the Uber Driver is Not At Fault (e.g., Pedestrian Accident or Cyclist Collision)

Similar to scenarios with another driver, if a pedestrian or cyclist is at fault for an accident with an Uber vehicle, their personal liability insurance (such as a renter's or homeowner's policy) may be pursued. If they have no insurance, the Uber driver or passengers might again turn to their own insurance or Uber's UM/UIM policy, depending on the specifics of the incident and the active insurance phase.

Special Considerations for Uber Passengers: Your Protections and Rights

Uber passengers are uniquely protected. Regardless of who is at fault for the accident—the Uber driver, another motorist, or a third party—passengers are typically covered. They can file a claim against the at-fault party's insurance. If the Uber driver is at fault, the $1 million liability policy applies. If another driver is at fault and underinsured, Uber's UM/UIM policy provides a crucial safety net for medical expenses and other damages.

Immediate Steps After an Uber Accident in California

The moments following a rideshare accident are chaotic and stressful. Taking the right steps can protect your health and any future insurance claims.

Prioritize Safety and Seek Medical Attention Immediately

Your first priority is safety. Move to a secure location if possible. Check yourself and others for injuries. Even if you feel fine, it's essential to seek a medical evaluation. Adrenaline can mask symptoms of serious injuries like whiplash or internal bleeding. Documenting your injuries early creates a medical record that is vital for your bodily injury claim.

Contact Authorities: The Importance of a Police Report

Call 911 immediately. Law enforcement will secure the scene, and the responding officer will create an official police report. This report is a critical piece of evidence for insurance claims, as it provides an objective account of the accident, identifies the parties involved, lists witnesses, and often includes a preliminary determination of fault.

Gather Crucial Evidence at the Scene

If you are physically able, gather as much evidence as possible.

- Photos and Videos: Document the accident scene, vehicle damage, license plates, road conditions, and any visible injuries.

- Information Exchange: Collect names, contact information, driver's license numbers, and insurance details from all drivers involved.

- Witness Contacts: Get the names and phone numbers of any witnesses. Their statements can be invaluable.

- Driver Status: If you are a passenger or another driver, confirm the Uber driver's status on the app (e.g., take a screenshot showing they were on an active trip).

Reporting the Accident to Uber Via the Uber App

Both drivers and passengers should report the accident to Uber as soon as possible. This can be done directly through the trip details section of the Uber app. This official notification creates a record of the incident and is the first step in initiating the Uber accident claim process with their insurance provider.

Navigating the Uber Accident Claim Process in California

Filing an insurance claim after a rideshare accident involves more steps than a standard car crash. Knowing who to contact and what to expect is key.

Initiating Your Claim: With Uber's Insurer or Your Own Auto Insurance?

Where you file your claim depends on the situation. If you are a passenger or a third party injured by an at-fault Uber driver on an active trip, you will file a claim directly with Uber's insurance company. If another driver was at fault, you would file with their insurer. Uber drivers may need to file claims with multiple insurers, including their own personal auto insurance (especially for collision coverage), Uber's insurer, and the at-fault driver's insurer.

Understanding Different Types of Damages and Compensation

An Uber accident claim can seek compensation for various damages, including:

- Economic Damages: Tangible losses such as current and future medical bills, lost wages, and property damage to your vehicle.

- Non-Economic Damages: Intangible losses like pain and suffering, emotional distress, and loss of enjoyment of life.

Dealing with Insurance Adjusters: What to Expect and How to Respond

Insurance adjusters represent the insurance company's interests, which is to minimize payouts. Be cautious in your communications. Provide factual information about the accident but avoid speculating on fault or the extent of your injuries. Never give a recorded statement without first consulting a personal injury attorney, as your words can be used against you later.

Potential Challenges: Navigating Denied Claims and Lowball Settlement Offers

Insurance companies may deny a claim by disputing liability or arguing that your injuries aren't related to the accident. They may also offer a quick, lowball settlement that doesn't fully cover your long-term medical expenses or other losses. It's important to understand the full value of your claim before accepting any offer.

The Role of California's At-Fault System in Your Uber Accident Claim

Because California is an at-fault state, proving the other party was negligent is central to your claim's success. Evidence from the police report, witness statements, and scene photos is crucial. If you share partial fault, California's "pure comparative negligence" rule allows you to still recover damages, but your compensation will be reduced by your percentage of fault.

California-Specific Legal Considerations for Uber Accidents

Navigating an Uber claim requires an understanding of California's unique legal landscape for ridesharing services.

Understanding the Statute of Limitations for Personal Injury Claims

In California, you generally have two years from the date of the accident to file a personal injury lawsuit. For property damage claims, the statute of limitations is three years. Missing these deadlines means you forfeit your right to seek compensation through the court system, making it critical to act promptly.

The Impact of California Law and Rideshare Regulations

California has been at the forefront of regulating ridesharing services. State law mandates the specific insurance minimums for each of Uber's operational phases. These regulations, like the requirement for a $1 million liability policy for TNCs, provide significant protection for the public but also add layers of legal complexity to any claim.

How Proposition 22 Affects Driver Classification and Insurance Claims

Passed in California, Proposition 22 classifies app-based drivers as independent contractors rather than employees. However, it also mandated that rideshare services provide certain benefits, including Occupational Accident Insurance for drivers. This insurance helps cover medical expenses and disability payments if a driver is injured while online, but it does not cover pain and suffering.

When to Consult a Personal Injury Attorney

While some minor accidents can be handled without legal help, consulting an attorney is often wise.

Why Uber Accident Claims Are More Complex Than Standard Auto Accidents

Uber accident claims involve navigating multiple insurance policies, dealing with large corporate insurers, and understanding specific state laws like Proposition 22. A personal injury attorney who specializes in rideshare accidents can manage these complexities, investigate the incident, accurately value your claim (including pain and suffering), and negotiate with insurers on your behalf to ensure you receive the full compensation you deserve. If you've suffered significant injuries, faced a denied claim, or received an unfair settlement offer, legal guidance is essential.

Conclusion

Navigating the aftermath of an Uber accident in California can be a daunting process. The key to a successful outcome lies in understanding the tiered insurance system based on the driver's app status, knowing who is liable, and taking immediate, decisive action after the crash. Prioritize your health, gather evidence, report the incident promptly, and be cautious when dealing with insurance adjusters.

For anything beyond a minor incident, the complexities of liability, multiple insurance policies, and California-specific regulations make professional legal advice invaluable. Consulting with a qualified personal injury attorney can help you protect your rights, accurately calculate your damages, and ensure you are not taken advantage of by large insurance corporations. By being informed and proactive, you can effectively navigate the claims process and focus on your recovery.