Introduction: The Financial Burden of Post-Accident Surgery in California

A severe car accident is a life-altering event, often leaving victims with significant injuries that require immediate and extensive medical care. When surgery becomes necessary, the physical and emotional trauma is compounded by a pressing financial question: who pays for it? In California, a state with a massive auto insurance market where direct premiums written for private passenger vehicles reached $36.49 billion in 2023, navigating the maze of insurance claims, medical bills, and legal liability can be overwhelming. This guide provides a clear path to understanding financial responsibility for surgery after a car accident in California.

Car Accidents and the Immediate Need for Surgery

The impact of a car crash can cause catastrophic harm, from complex bone fractures and internal bleeding to traumatic brain and spinal cord injuries. These conditions often demand emergency surgical intervention to stabilize the patient, repair damage, and prevent long-term complications. The urgency of these procedures means there is no time to determine fault or negotiate with insurance companies; the priority is saving life and limb. This immediate need for high-cost medical care creates an instant financial crisis for the injured party.

Understanding California's Fault-Based System and Liability

California operates under a "fault" or "at-fault" insurance system. This means the person who is legally responsible for causing the accident is also responsible for the damages that result, including all related medical expenses. In theory, the at-fault driver’s auto liability insurance should cover the cost of your surgery. However, this is where the complexity begins. Liability isn't automatic; it must be proven.

Why Navigating Surgical Costs After a Car Wreck is Complex

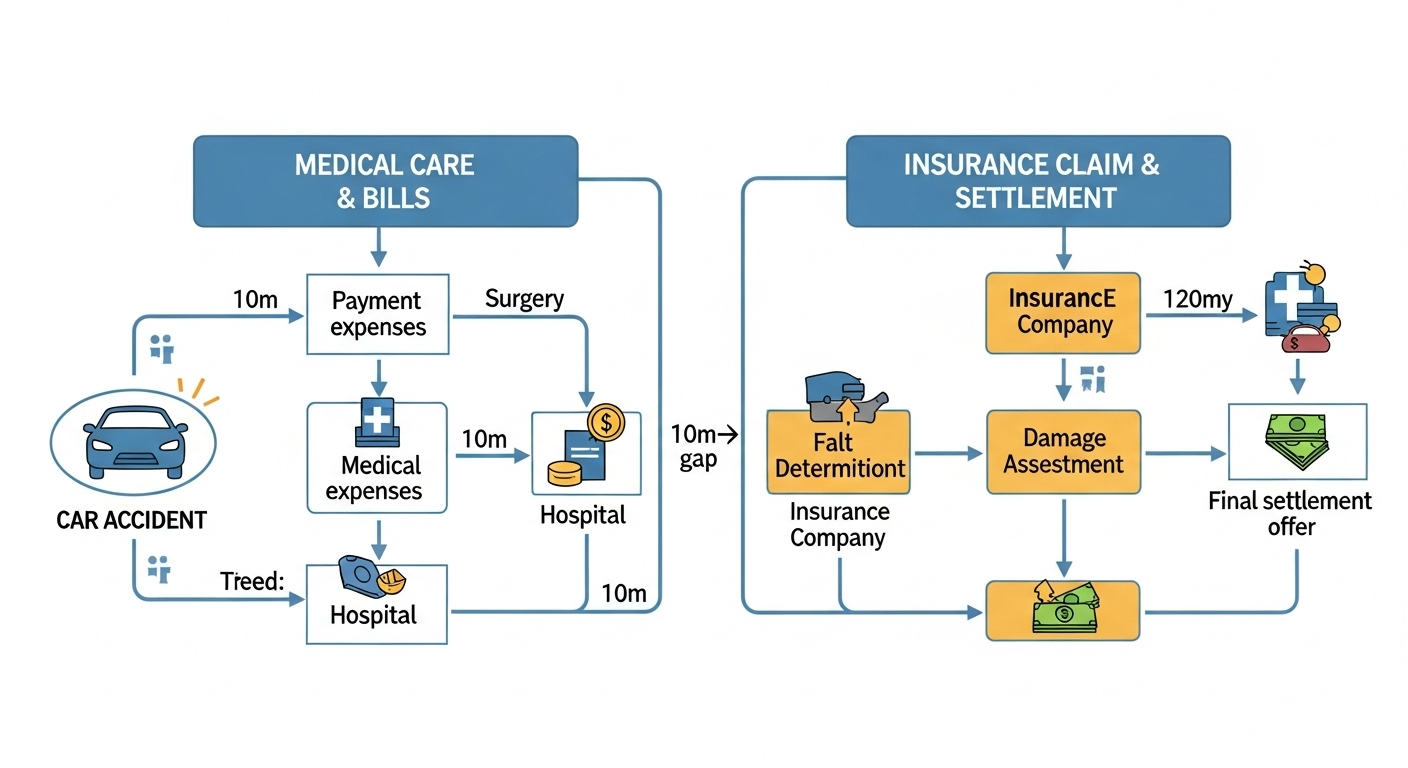

Timeline of expenses and insurance settlement after a car accident requiring surgery in California. Note the significant delay between incurring medical costs and receiving an insurance settlement.

The primary challenge is timing. While the at-fault driver is ultimately liable, their insurance company will not pay your medical bills as they come in. They will investigate the claim, determine fault, assess the extent of your damages, and then typically make a single lump-sum settlement offer. This process can take months, or even years, especially if liability is disputed. Meanwhile, the hospital, surgeons, and anesthesiologists expect payment for the surgery now. This gap between the immediate need for payment and the delayed settlement is the central problem victims face.

Immediate Solutions: How to Secure Necessary Surgery Without Upfront Payment

While you pursue a personal injury claim against the at-fault driver, you need a way to cover the immediate, and often staggering, cost of surgery. Fortunately, several options exist to ensure you get the care you need without waiting for a settlement.

Utilizing Your Own Health Insurance (Private, Medicare, Medi-Cal)

Your first line of defense is your own health insurance policy, whether it’s a private plan, Medicare, or Medi-Cal. Your health insurer is contractually obligated to cover your medical care, including emergency surgery, regardless of how the injury occurred. You will be responsible for your deductible, co-pays, and any out-of-network costs, but the bulk of the surgical bill will be covered. It's crucial to understand that your health insurance company will later seek reimbursement from the at-fault driver's insurance settlement through a process called subrogation.

Medical Payments (MedPay) Coverage Through Your Auto Insurance Policy

Medical Payments coverage, or MedPay, is an optional part of your own auto insurance policy in California. It covers medical expenses for you and your passengers after an accident, regardless of who was at fault. MedPay has set limits, typically ranging from $1,000 to $10,000 or more. While it may not cover the entire cost of a major surgery, it can be invaluable for covering deductibles, co-pays, or initial emergency room expenses, providing immediate financial relief.

Medical Liens and Letters of Protection (LOPs)

What if you don't have health insurance, or your policy has high out-of-pocket costs? A medical lien may be the solution. A medical lien is a legal agreement between you, your attorney, and your medical provider. The provider agrees to perform the surgery and delay payment until your personal injury case is resolved. In exchange, they place a lien on your future settlement, guaranteeing they will be paid from those funds. An attorney often facilitates this by sending the provider a "Letter of Protection" (LOP), which formalizes the arrangement. This allows you to get critical surgical care based on the strength of your personal injury claim.

Worker's Compensation and Surgical Costs (If Applicable)

If your car accident occurred while you were on the job—for example, if you were a delivery driver or traveling for a work-related meeting—you may be eligible for workers' compensation benefits. This system is designed to cover all medical expenses related to a workplace injury, including surgery, without requiring you to prove fault. Your workers' compensation claim would be the primary source for covering your surgical costs in this scenario.

Primary Responsibility: The At-Fault Driver's Insurance

While immediate payment options are critical for getting care, the ultimate financial responsibility rests with the party who caused the accident. Securing compensation from their insurance company is the end goal of your personal injury claim.

Establishing Fault and Negligence Under California Law

To hold the other driver financially responsible, you or your attorney must prove they were negligent. Negligence means they failed to exercise reasonable care, and this failure caused your injuries. This is established by investigating the accident, gathering evidence like police reports and witness statements, and demonstrating a direct link between the other driver’s actions—such as speeding or distracted driving—and your need for surgery. For instance, data from 2024 shows speeding was a factor in 77,822 accidents in California, underscoring how common negligent behavior leads to serious crashes.

The At-Fault Driver's Auto Liability Insurance Policy

Every driver in California is required to carry minimum liability insurance coverage. This policy is what pays for the damages—including medical expenses for surgery—that their insured driver causes to others. Once your personal injury claim is settled or a verdict is won, the at-fault driver's insurance company will issue a payment to cover your documented economic and non-economic damages up to their policy limits.

What If the At-Fault Driver is Uninsured or Underinsured?

This is a distressingly common scenario. According to 2022 insurance data, California has the 11th-highest rate of uninsured drivers, with about 17% of motorists lacking required coverage. If the at-fault driver has no insurance, you can turn to your own Uninsured Motorist (UM) coverage. If their coverage limits are too low to cover your surgical costs, your Underinsured Motorist (UIM) coverage can bridge the gap. UM/UIM coverage is not mandatory in California, but it is a vital protection that insurance companies must offer.

Deconstructing Surgical Costs: Beyond the Operation Itself

The total cost of surgery extends far beyond the surgeon's fee. To ensure you receive full compensation, it's essential to account for every related expense in your personal injury claim.

Common Injuries in California Car Accidents Requiring Surgery

High-impact collisions frequently result in severe injuries that necessitate surgical repair. Common examples include:

- Orthopedic Surgery: For compound fractures, shattered bones (especially in the legs, hips, and arms), and joint reconstruction.

- Spinal Surgery: Procedures like spinal fusions or discectomies to address herniated discs or vertebral fractures.

- Neurosurgery: To relieve pressure on the brain from swelling or bleeding after a traumatic brain injury.

- Internal Surgery: To repair damage to organs like the spleen, liver, or bowels.

Comprehensive Breakdown of Surgical Expenses

A complete accounting of surgical damages in your claim should include:

- Surgeon and assistant surgeon fees

- Anesthesiologist fees

- Hospital or surgical facility costs (operating room, recovery room)

- Medical imaging (X-rays, MRIs, CT scans) pre- and post-operation

- Implanted hardware (plates, screws, rods)

- Post-operative hospital stays

- Medications and pain management

Accounting for Future Surgical Needs and Long-Term Medical Expenses

Your initial surgery may not be the last. Your settlement must also account for potential future medical needs. This could include a second surgery to remove hardware, scar revision procedures, or joint replacement surgery years down the line. It also includes long-term costs like physical therapy, rehabilitation, prescription medications, and necessary home modifications. A qualified personal injury attorney will work with medical experts to project these future costs and include them in your demand for damages.

Navigating Complexities: Subrogation, Deductibles, and Maximizing Recovery

The interaction between different insurance policies and payment methods can be complex. Understanding these processes is key to protecting your final settlement.

The Interplay Between Health Insurance, MedPay, and Auto Liability Coverage for Surgical Bills

Think of these as layers of coverage. MedPay can cover your initial out-of-pocket costs. Your health insurance then pays the bulk of the surgical bills. Finally, the settlement from the at-fault driver's liability insurance is used to reimburse your health insurer and cover all other damages. Coordinating these sources correctly ensures your bills are paid promptly while preserving your right to full compensation.

Understanding Subrogation and the Reimbursement Process for Surgical Bills

Subrogation is the legal right of your health insurance company to recover the money it paid for your surgery from the at-fault party. When you receive your settlement, your health insurer will have a claim on a portion of it to be reimbursed. This process prevents you from "double-dipping"—having your bills paid by both health insurance and the settlement.

Out-of-Pocket Expenses and Deductibles Related to Surgery

Even with good insurance, you will likely incur out-of-pocket expenses. These include your health insurance deductible, co-payments for appointments and prescriptions, and the cost of any treatments not fully covered. These are all considered part of your damages and should be meticulously tracked and included in your personal injury claim for reimbursement.

Protecting Your Settlement Offer from Excessive Medical Liens and Claims

When your settlement arrives, various parties will seek payment, including health insurers (subrogation) and medical providers (liens). An experienced attorney is crucial here. They can negotiate with lienholders to reduce the amount they are owed, ensuring that more of the settlement money goes into your pocket to compensate you for your pain, suffering, and future needs.

The Indispensable Role of a California Personal Injury Attorney

When facing surgery after a car accident, navigating the financial and legal aftermath on your own is a monumental task. A skilled personal injury attorney becomes your most important advocate.

Why an Injury Lawyer is Crucial When Facing Significant Surgical Bills

An attorney understands the complex interplay between medical treatment and legal claims. They can connect you with medical providers who work on a lien basis, ensuring you get the surgery you need immediately. They handle all communications with insurance companies, protecting you from tactics designed to devalue your claim.

Negotiating with Insurance Companies and Medical Providers

Insurance adjusters are trained to minimize payouts. An attorney levels the playing field, using their knowledge of California law and evidence from your case to negotiate a fair settlement. The average car accident settlement in California is around $29,700 for injured drivers, but cases involving surgery can be worth significantly more. An attorney also negotiates with lienholders after a settlement to reduce your repayment obligations.

Proving Damages for Past and Future Surgical Costs

A lawyer works with medical and economic experts to build a comprehensive case for damages. They will gather all medical records and bills to prove past expenses and use expert testimony to create a detailed life care plan that calculates the cost of all future medical needs related to your surgery.

Filing a Personal Injury Lawsuit if a Fair Settlement Offer Cannot Be Reached

If the insurance company refuses to offer a fair settlement, your attorney will be prepared to file a lawsuit and take your case to court. The willingness and ability to litigate a case often pressure insurance companies to negotiate in good faith and offer a more reasonable settlement.

Expert Opinions and Medical Documentation for Surgical Necessity

A key part of your claim is proving that the surgery was medically necessary and a direct result of the car accident. An attorney works closely with your treating physicians to obtain clear, compelling documentation and expert opinions that establish this causal link, leaving no room for the insurance company to dispute the claim.

Your Action Plan: Steps After a Car Accident Requiring Surgery

If you or a loved one requires surgery after a California car accident, the path to financial recovery can seem daunting, but it is manageable with the right approach. Your immediate priority is always your health; seek all necessary medical care without delay. Use your health insurance or MedPay to cover upfront costs. Preserve all evidence from the accident scene, document your injuries meticulously, and track every single expense. Most importantly, consult with an experienced California personal injury attorney. They can manage the complexities of your claim, negotiate with insurance companies, and ensure you receive the financial resources necessary to cover your surgery and rebuild your life. By understanding your rights and the resources available, you can focus on what matters most: your recovery.